Ever thought about living in the same house with your grandparents, parents, or other loved ones? You're not alone. A lot of people are choosing to buy multi-generational homes where everyone can live together. Let's check out why they think it’s a good idea to see if it might be a good fit for you, too. Why People Are Choosing Multi-Generational LivingAccording to the National Association of Realtors (NAR), here are just a few key reasons buyers opted for multi-generational homes over the past year (see graph below):  Two of the top reasons had to do with aging parents. 27% of buyers chose multi-generational homes so they could take care of their parents more easily. And 19% did it to spend more time with them. A lot of older adults want to age in place, and living in a home with loved ones can help them do just that. If your parents are hoping to do the same, but need a bit of help, a multi-generational home may be worth considering.

But buying a multi-generational home isn’t just about being close or taking care of the people you love—it can save you money, too. 22% of buyers say they picked a multi-generational home to cut down on costs, and 11% needed a bigger house multiple incomes could afford together. Sharing costs like the mortgage and utilities can make owning a home more affordable. This is especially helpful for first-time homebuyers who might find it challenging to buy a place on their own in today's market. As Axios explains: “Financial concerns and caregiving needs are two of the major reasons people live with their parents (and parents’ parents).” How an Agent Is Key in Finding the Right Home for YouLooking for the perfect multi-generational home is a bit trickier than finding a regular house. You've got more people, which means more opinions and needs to think about. It's kind of like putting together a puzzle where all the pieces need to fit perfectly. If you're into the idea of living with loved ones and want all the benefits that come with it, team up with a local real estate agent who can help you out. Bottom LineWhether you're looking to save money or want to take care of your loved ones, buying a multi-generational home might be a good idea for you. If you want to find out more, let’s talk.

0 Comments

The number of homes for sale is playing a big role in today’s housing market. And, if you’re considering whether or not to list your house, today’s limited supply is one of the biggest advantages you have right now. That’s because your house stands out more when the inventory is low, especially if it’s priced right. But the supply of homes for sale is growing. According to the latest data from Realtor.com, new listings (homeowners who just put their house up for sale) are trending up (see graph below):  This graph shows more homeowners are putting that sale sign up in their yards compared to the same time last year. As Realtor.com says:

“. . . sellers turned out in higher numbers this March as newly listed homes were 15.5% above last year’s levels. This marked the fifth month of increasing listing activity after a 17-month streak of decline.” What This Means for YouIf you’ve been putting off selling your house, maybe it’s time to start thinking about it again – before your neighbors do. While we’re not going to suddenly have a surplus of homes for sale, each house that pops on the market in your area runs the risk of pulling buyer attention away from yours. For example, if your neighbor gets in on the action and lists their house too, it means you’ll have competition right next door. You don’t want buyers to tour your house and fall in love with someone else’s. You want yours to be in the spotlight. A great agent can make that happen. They’ll help you get your house ready to list, draw attention to everything today’s buyers are looking for, and help you price it right. That way buyers are really drawn to your listing and eager to make it their home. If you’re ready and able to sell now, here’s your chance to get the best of both worlds. Since the supply of homes for sale is growing, you’ll have more options for your own move. But you’ll also be able to sell while your house will still stand out. Bottom LineEven though inventory is still low, you don’t want to wait for more competition to pop up in your neighborhood. Let’s connect to go over the perks of selling before more homes come to the market.  Thinking about buying a home? While today’s mortgage rates might seem a bit intimidating, here are two solid reasons why, if you’re ready and able, it could still be a smart move to get your own place. 1. Home Values Typically Go Up Over TimeThere’s been some confusion over the past year or so about which way home prices are headed. Make no mistake, nationally they’re still going up. In fact, over the long-term, home prices almost always go up (see graph below):  Using data from the Federal Reserve (the Fed), you can see the overall trend is home prices have climbed steadily for the past 60 years. There was an exception during the 2008 housing crash when prices didn't follow the normal pattern, but generally, home values kept rising. This is a big reason why buying a home can be better than renting. As prices go up and you pay down your mortgage, you build equity. Over time, this growing equity can really increase your net worth. The Urban Institute says: “Homeownership is critical for wealth building and financial stability.” 2. Rent Keeps Rising in the Long RunHere’s another reason you may want to think about buying a home instead of renting – rent just keeps going up over the years. Sure, it might be cheaper to rent right now in some areas, but every time you renew your lease or sign a new one, you’re likely to feel the squeeze of your rent getting higher. According to data from iProperty Management, rent has been going up pretty consistently for the last 60 years, too (see graph below):  So how do you escape the cycle of rising rents? Buying a home with a fixed-rate mortgage helps you stabilize your housing costs and say goodbye to those annoying rent increases. That kind of stability is a big deal.

Your housing payments are like an investment, and you've got a decision to make. Do you want to invest in yourself or keep paying your landlord? When you own your home, you're investing in your own future. And even when renting is cheaper, that money you pay every month is gone for good. As Dr. Jessica Lautz, Deputy Chief Economist and VP of Research at the National Association of Realtors (NAR), says: “If a homebuyer is financially stable, able to manage monthly mortgage costs and can handle the associated household maintenance expenses, then it makes sense to purchase a home.”Bottom LineIf you're tired of your rent going up and want to explore the many benefits of homeownership, let’s talk to explore your options.  Tips for Younger Homebuyers: How To Make Your Dream a Reality

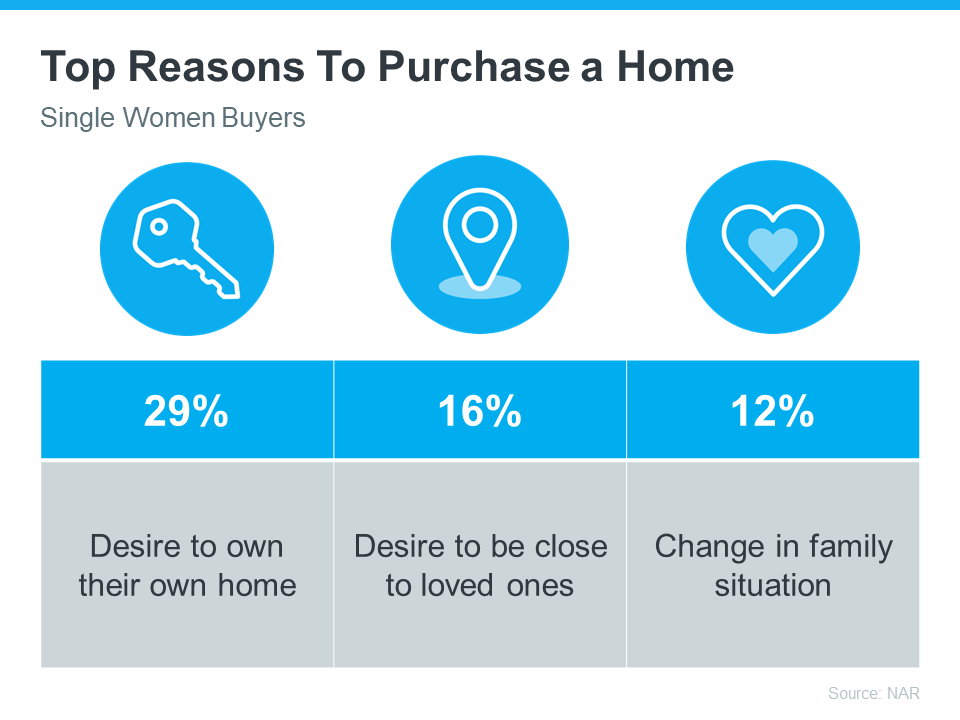

If you’re a member of a younger generation, like Gen Z, you may be asking the question: will I ever be able to buy a home? And chances are, you’re worried that’s not going to be in the cards with inflation, rising home prices, mortgage rates, and more seemingly stacked against you. While there’s no arguing this housing market is challenging for first-time homebuyers, it is still achievable, especially if you have professionals on your side. Here are some helpful tips you may get from a pro. 1. Explore Your Options for a Down PaymentIf a down payment is your #1 hurdle, you may have options to give your savings a boost. There are over 2,000 down payment assistance programs designed to make homeownership more achievable. And, that’s not the only place you may be able to get a helping hand. While it may not be an option for everyone, 49% of Gen Z homebuyers got money from loved ones that they used toward a down payment, according to LendingTree. And chances are you won’t need to put 20% down (unless specified by your loan type or lender). So be sure to work with a trusted mortgage professional to explore your options, find out how much you’ll really need, and learn about any guidelines on getting a gift from loved ones. 2. Live with Loved Ones To Boost Your SavingsAnother thing a number of Gen Z buyers are doing is ditching their rental and moving back in with friends or family. This can help cut down your housing costs so you can build your savings a whole lot faster. As Bankrate explains: “. . . many have opted to stop renting and live with family in order to boost their savings. Thirty percent of Gen Z homebuyers move directly from their family member’s home to a home of their own, according to NAR.” 3. Cast a Broad Net for Your SearchWhen you’ve saved up enough, here’s how a pro will help you approach your search. Since the supply of homes for sale is still low and affordability is tight, they’ll give you strategies and avenues you may not have considered to open up your pool of options. For example, it’s usually more affordable if you consider a rural or suburban area versus an urban one. So, while the city may be livelier and more energetic, the cost of living may be reason enough to look at something further out. And if you consider smaller homes and condos or townhouses, you’ll give yourself even more ways to break into the market. As Colby Stout, Research Analyst at Bright MLS, explains: “Being flexible on the types of home (e.g., a condo or townhome versus a single-family home) and exploring more affordable neighborhoods is important for first-time buyers.” 4. Take a Close Look at Your Wants and NeedsAnd lastly, an agent can help you really think about your must-have’s and nice-to-have’s. Remember, your first home doesn’t have to be your forever home. You just need to get your foot in the door to start building equity. If you want to buy, you may find making some compromises is worth it. As Chase says: “An open-minded approach to house-hunting may be one way for Gen Z homebuyers to maintain some edge. This could mean buying in areas that are less expensive. Differentiating needs vs. wants may help in this area as well.”An agent will help you prioritize your list of home features and find houses that can deliver on the top ones. And they’ll be able to explain how equity can benefit you in the long run and make it possible to move into that dream home down the line. Bottom LineReal estate professionals have expertise on what’s working for other buyers like you. Lean on them for tips and advice along the way. As Directors Mortgage says, with that support you can make it happen: “The path to homeownership may not be a straightforward one for Gen Z, but it’s undoubtedly within reach. By adopting the right strategies, like exploring down payment assistance programs and sharing living costs with relatives, you can bring your dream of owning a home closer to reality.” Let’s connect to get you set up for long-term success.  In today's housing market, more and more single women are becoming homeowners. According to data from the National Association of Realtors (NAR), 19% of all homebuyers are single women, while only 10% are single men. If you're a single woman trying to buy your first home, this should be encouraging. It means other people are making their dreams a reality – so you can too. Why Homeownership Matters to So Many WomenFor many single women, buying a home isn't just about having a place to live—it's also a smart way to invest for the future. Homes usually increase in value over time, so they’re a great way to build equity and overall net worth. Ksenia Potapov, Economist at First American, says: “. . . single women are increasingly pursuing homeownership and reaping its wealth creation benefits.”The financial security and independence homeownership provides can be life-changing. And when you factor in the personal motivations behind buying a home, that impact becomes even clearer. The same report from NAR shares the top reasons single women are buying a home right now, and the reality is, they’re not all financial (see chart below):  If any of these reasons resonate with you, maybe it’s time for you to buy too.

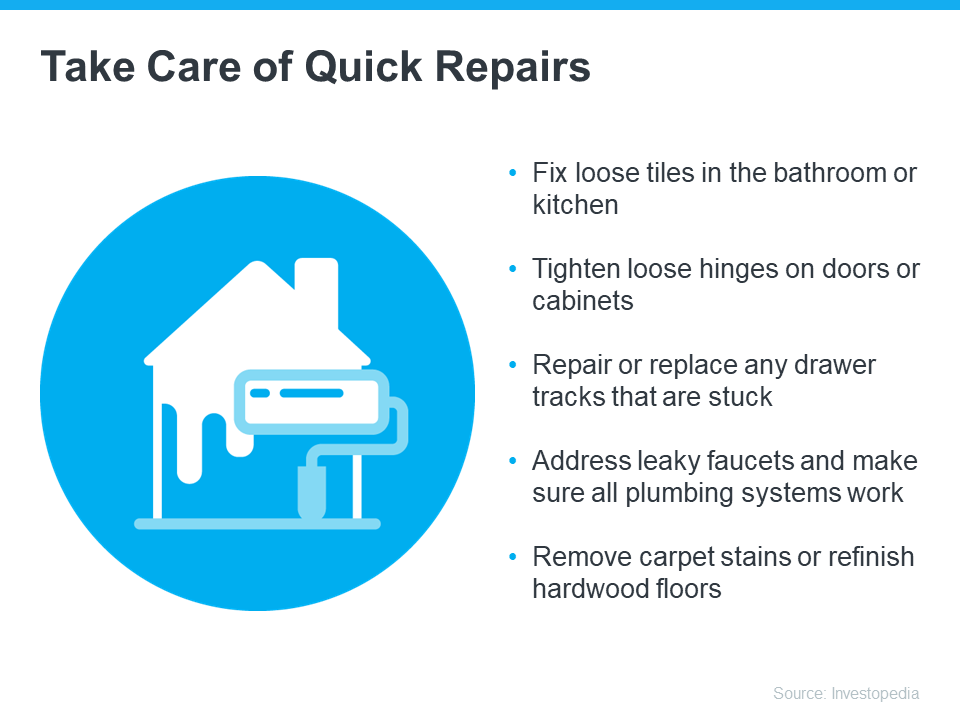

Work with a Trusted Real Estate AgentIf you’re a single woman looking to buy a home, it is possible, even in today’s housing market. You’ll just want to be sure you have a great real estate agent by your side. Talk about what your goals are and why homeownership is so important to you. That way your agent can keep what’s critical for you up front as they guide you through the buying process. They’ll help you find the right home for your needs and advocate for you during negotiations. Together, you can make your dream of homeownership a reality. Bottom LineHomeownership is life-changing no matter who you are. Let's connect today to talk about your goals in the housing market.  The Best Week To List Your House Is Almost Here Are you thinking about making a move? If so, now may be the perfect time to start the process. That’s because experts say the best week to list your house is just around the corner. A recent Realtor.com study looked at housing market trends over the past several years (with the exception of 2020, since it was an unusual year), and found the best week to put your house on the market this year is April 14-20: “Every year, one week stands out from the rest as that perfect stretch of time when it’s great to be a home seller. This year, the week of April 14–20 is the best time to sell—that is, if sellers want to see lots of interest in their homes, sell quickly, and pocket some extra cash, according to Realtor.com® data.” Here’s why this matters for you. While the spring market is a great time to sell no matter the week, this may be the peak sweet spot. And if you’ve been putting your plans on the back burner and waiting for the right time to act, this could be the nudge you need to make your move happen. As Hannah Jones, Senior Economic Research Analyst at Realtor.com explains: “The third week of April brings the best combination of housing market factors for sellers. The best week offers higher buyer demand, lower competition [from other sellers], and fewer price reductions than the typical week of the year.” But, if you want to get in on the action, you’ll need to move quickly and lean on the pros. Your local real estate agent is the perfect go-to when it comes to figuring out a plan to prep your house and get it on the market. They’ll be able to offer advice to balance your target listing date with what you need to do from a repair and renovation standpoint. And they can walk you through exactly how to prioritize your list so you know what to tackle first. For example, if your house is already in good shape, you’ll be able to really focus in on the smaller things that are easy to do and make a big impact. As an article from Investopedia says: “You won’t have time for any major renovations, so focus on quick repairs to address things that could deter potential buyers.”Here are some specific examples from that article:  Just remember, even if you’re not ready to list within the next couple of weeks, that’s okay. The window of opportunity doesn’t close when this week ends. Spring is the peak homebuying season and it’s still a seller’s market, so you’ll be in the driver’s seat all season long.

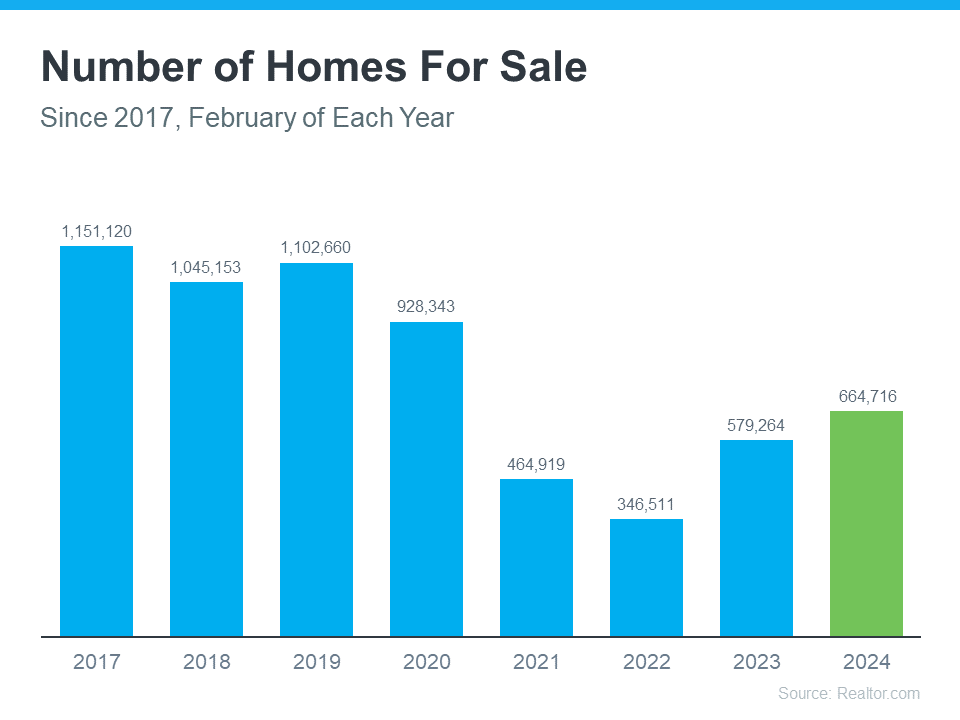

Bottom LineReady to get the ball rolling? Let’s connect and schedule a time to go over your next steps.  One of the biggest hurdles buyers have faced over the past few years has been a lack of homes available for sale. But that’s starting to change. The graph below uses the latest data from Realtor.com to show there are more homes on the market in 2024 than there have been in any of the past several years (2021-2023):  Does That Mean Finding a Home Is Easier?The answer is yes, and no. As an article from Realtor.com says:

“There were nearly 15% more homes for sale in February than a year earlier . . . That alone could jolt the housing market a bit if more “For Sale” signs continue to appear. However, the nation is still suffering from a housing shortage even with all of that new inventory.”Context is important. On the one hand, inventory is up over the past few years. That means you’ll likely have more options to choose from as you search for your next home. But, at the same time, the graph above also shows there are still significantly fewer homes for sale than there would usually be in a more normal, pre-pandemic market. And that deficit isn’t going to be reversed overnight. What Does This Mean for You?You might find a few more choices now than in recent years, but you shouldn’t expect a ton of options. To help you explore the growing list of choices you have now, team up with a local real estate agent you trust. They can really help you understand the inventory situation where you want to buy. That’s because real estate is local. An experienced agent can share some smart tips they’ve used to help other buyers in your area deal with ongoing low housing supply. Bottom LineIf you’re thinking about buying a home, let’s team up. That way, you’ll be up to date on everything that could affect your move, including how many homes are for sale right now.  If you’re trying to sell your house, you may be looking at this spring season as the sweet spot – and you’re not wrong. We’re still in a seller’s market because there are so few homes for sale right now. And historically, this is the time of year when more buyers move, and competition ticks up. That makes this an exciting time to put up that for sale sign.

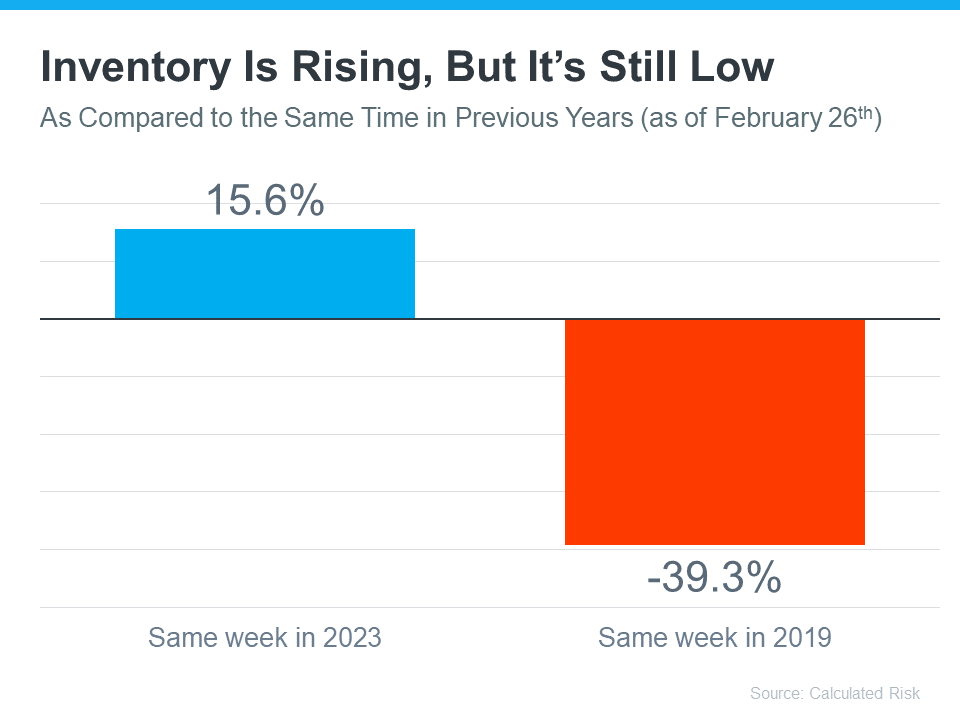

But while conditions are great for sellers like you, you’ll still want to be strategic when it comes time to set your asking price. That’s because pricing your house too high may actually cost you in the long run. The Downside of Overpricing Your HouseThe asking price for your house sends a message to potential buyers. From the moment they see your listing, the price and the photos are what’s going to make the biggest first impression. And, if it’s priced too high, you may turn people away. As an article from U.S. News Real Estate says: “Even in a hot market where there are more buyers than houses available for sale, buyers aren't going to pay attention to a home with an inflated asking price.”That’s because no homebuyer wants to pay more than they have to, especially not today. Many are already feeling the pinch on their budget due to ongoing home price appreciation and today’s mortgage rates. And if they think your house is overpriced, they may write it off without even stepping foot in the front door, or simply won’t make an offer if they think it’s priced too high. If that happens, it’s going to take longer to sell. And ideally you don’t want to have to think about doing a price drop to try to re-ignite interest in your house. Why? Some buyers will see the price cut as a red flag and wonder why the price was reduced, or they’ll think something is wrong with the house the longer it sits. As an article from Forbes explains: “It’s not only the price of an overpriced home that turns buyers off. There’s also another negative component that kicks in. . . . if your listing just sits there and accumulates days on the market, it will not be a good look. . . . buyers won’t necessarily ask anyone what’s wrong with the home. They’ll just assume that something is indeed wrong, and will skip over the property and view more recent listings.” Your Agent’s Role in Setting the Right PriceInstead, pricing it at or just below current market value from the start is a much better strategy. So how do you find that ideal asking price? You lean on the pros. Only an agent has the expertise needed to research and figure out the current market value for your home. They’ll factor in the condition of your house, any upgrades you’ve made, and what other houses like yours are selling for in your area. And they’ll use all of that information to find that target number. The right price will bring in more buyers and make it more likely you’ll see multiple offers too. Plus, when homes are priced right, they still tend to sell quickly. Bottom LineEven though you want to bring in top dollar when you sell, setting the asking price too high may deter buyers and slow down the sales process. Let’s connect to find the right price for your house, so we can maximize your profit and still draw in eager buyers willing to make competitive offers.  Buying a home this spring? You’re probably navigating today’s affordability challenges and dealing with the limited number of homes for sale. But, what if there was a solution that could help with both? If you’re having a hard time finding a home you love, and mortgage rates are putting pressure on your budget, it may be time to look at newly built homes. Here’s why. New Home Construction Is an Inventory Bright Spot When looking for a home, you can choose between existing homes (those that are already built and previously owned) and newly constructed ones. While the number of existing homes for sale has increased this year, there are still fewer available than there were in more typical years in the housing market, like back in 2018 or 2019. So, if you’re looking to expand your pool of options even more, turning to newly built homes can help. As Danielle Hale, Chief Economist at Realtor.com, explains: “The shortage of existing homes For Sale has opened up the possibility of new-home construction to more buyers who may not have once considered it.”And the good news is, there are more newly built homes to pick from right now. The graphs below use data from the Census to show how new home construction is ramping up in two key areas (see most recent spike in green): Starts, or homes where builders just broke ground, have seen a big increase lately. And completions, homes that builders just finished, are also up significantly. So, if you want a new, move-in ready home or you want to get in early and customize your build along the way, you have more options right now. Builders Are Offering Incentives To Help with Affordability And to sweeten the pot, builders are offering things like mortgage rate buy-downs and other perks for homebuyers right now. This can help offset today’s affordability challenges while also getting you into your dream home. Mark Fleming, Chief Economist at First American, explains why you may find builders have more wiggle room to offer more for you than the typical homeowner: “Builders aren't rate locked-in. They would love to sell you the home because they're not living in it. It costs money not to sell the home. And many of the public home builders have said in their earnings calls that they are not going to be pulling back on incentives, especially the mortgage rate buydown, so that will help the new-home market continue to perform well in the spring home-buying season. ”An article from HousingWire also says this about what builders are offering right now: ". . . the use of sales incentives still shows some momentum as 60% of respondents reported using them, up from 58% in February. " Just remember, buying from a builder is different from buying from a home seller, so it’s important to partner with a local real estate agent. Builder contracts can be complex. A trusted agent will be your advocate throughout the process. They’ll be your go-to resource for advice on construction quality and builder reputation, reviewing and negotiating contracts to get you the best deal, helping you decide on which customizations and upgrades are most worthwhile, and a whole lot more. Bottom LineIf you’re struggling to find a home to buy, or with today’s affordability challenges, let’s connect to see if newly built homes could be the solution you’re looking for.  Wondering if it still makes sense to sell your house right now? The short answer is, yes. And if you look at the current number of homes for sale, you’ll see two reasons why. An article from Calculated Risk shows there are 15.6% more homes for sale now compared to the same week last year. That tells us inventory has grown. But going back to 2019, the last normal year in the housing market, there are nearly 40% fewer homes available now:  Here’s a breakdown of how this benefits you when you sell.

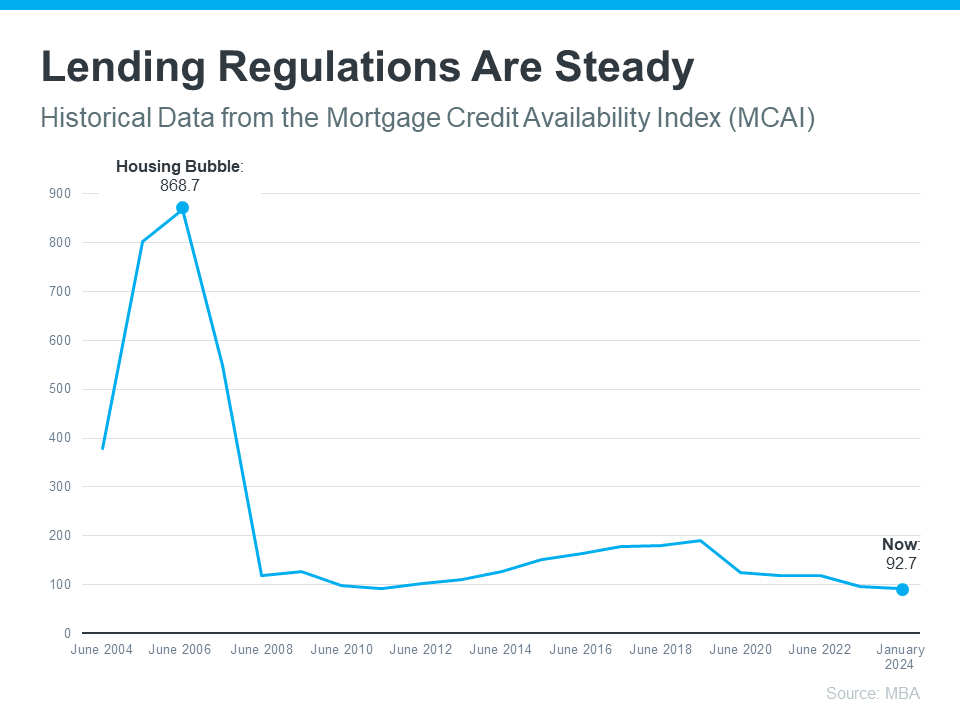

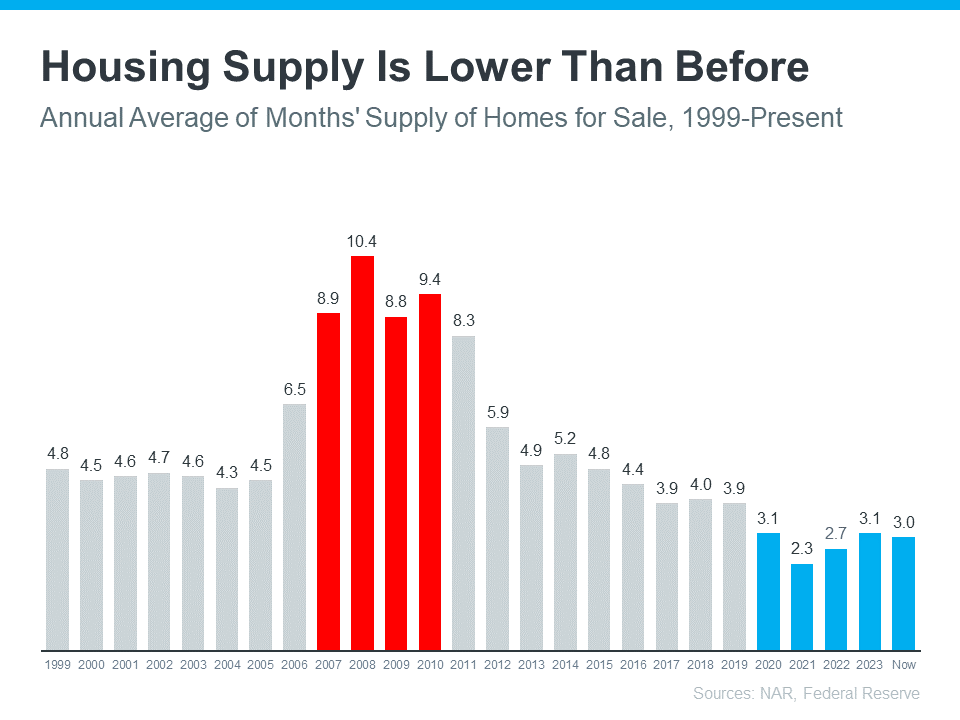

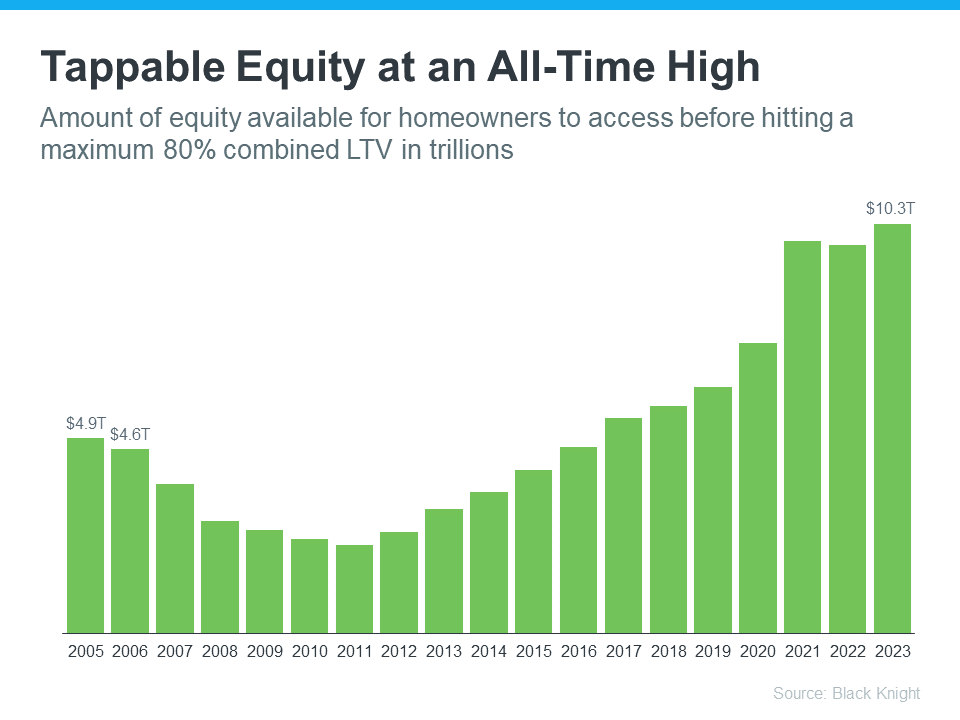

1. You Have More Options for Your MoveAre you thinking about selling because your current house is too big, too small, or because your needs have changed? If so, the year-over-year growth gives you more options for your home search. That means it may be less of a challenge to find what you’re looking for. So, if you were holding off on selling because you were worried you weren’t going to find a home you like, this may be just the good news you needed. Partnering with a local real estate professional can help you make sure you’re up to date on the homes available in your area. 2. You Still Won’t Have Much Competition When You SellBut to put that into perspective, even though there are more homes for sale now, there still aren’t as many as there’d be in a normal year. Remember, the data from Calculated Risk shows we’re down nearly 40% compared to 2019. And that large a deficit won't be solved overnight. As a recent article from Realtor.com explains: “. . . the number of homes for sale and new listing activity continues to improve compared to last year. However the inventory of homes for sale still has a long journey back to pre-pandemic levels.”For you, that means if you work with an agent to price your house right, it should still get a lot of attention from eager buyers and could sell fast. Bottom LineIf you're a homeowner looking to sell, now's a good time. You'll have more options when buying your next home, and there's still not a ton of competition from other sellers. If you’re ready to move, let’s connect to get the ball rolling.  If you’re holding out hope that the housing market is going to crash and bring home prices back down, here’s a look at what the data shows. And spoiler alert: that’s not in the cards. Instead, experts say home prices are going to keep going up. Today’s market is very different than it was before the housing crash in 2008. Here’s why. It’s Harder To Get a Loan Now – and That’s Actually a Good ThingIt was much easier to get a home loan during the lead-up to the 2008 housing crisis than it is today. Back then, banks had different lending standards, making it easy for just about anyone to qualify for a home loan or refinance an existing one. Things are different today. Homebuyers face increasingly higher standards from mortgage companies. The graph below uses data from the Mortgage Bankers Association (MBA) to show this difference. The lower the number, the harder it is to get a mortgage. The higher the number, the easier it is:  The peak in the graph shows that, back then, lending standards weren’t as strict as they are now. That means lending institutions took on much greater risk in both the person and the mortgage products offered around the crash. That led to mass defaults and a flood of foreclosures coming onto the market. There Are Far Fewer Homes for Sale Today, so Prices Won’t CrashBecause there were too many homes for sale during the housing crisis (many of which were short sales and foreclosures), that caused home prices to fall dramatically. But today, there’s an inventory shortage – not a surplus. The graph below uses data from the National Association of Realtors (NAR) and the Federal Reserve to show how the months’ supply of homes available now (shown in blue) compares to the crash (shown in red)  Today, unsold inventory sits at just a 3.0-months’ supply. That’s compared to the peak of 10.4 month’s supply back in 2008. That means there’s nowhere near enough inventory on the market for home prices to come crashing down like they did back then. People Are Not Using Their Homes as ATMs Like They Did in the Early 2000sBack in the lead up to the housing crash, many homeowners were borrowing against the equity in their homes to finance new cars, boats, and vacations. So, when prices started to fall, as inventory rose too high, many of those homeowners found themselves underwater. But today, homeowners are a lot more cautious. Even though prices have skyrocketed in the past few years, homeowners aren’t tapping into their equity the way they did back then. Black Knight reports that tappable equity (the amount of equity available for homeowners to access before hitting a maximum 80% loan-to-value ratio, or LTV) has actually reached an all-time high:  That means, as a whole, homeowners have more equity available than ever before. And that’s great. Homeowners are in a much stronger position today than in the early 2000s. That same report from Black Knight goes on to explain:

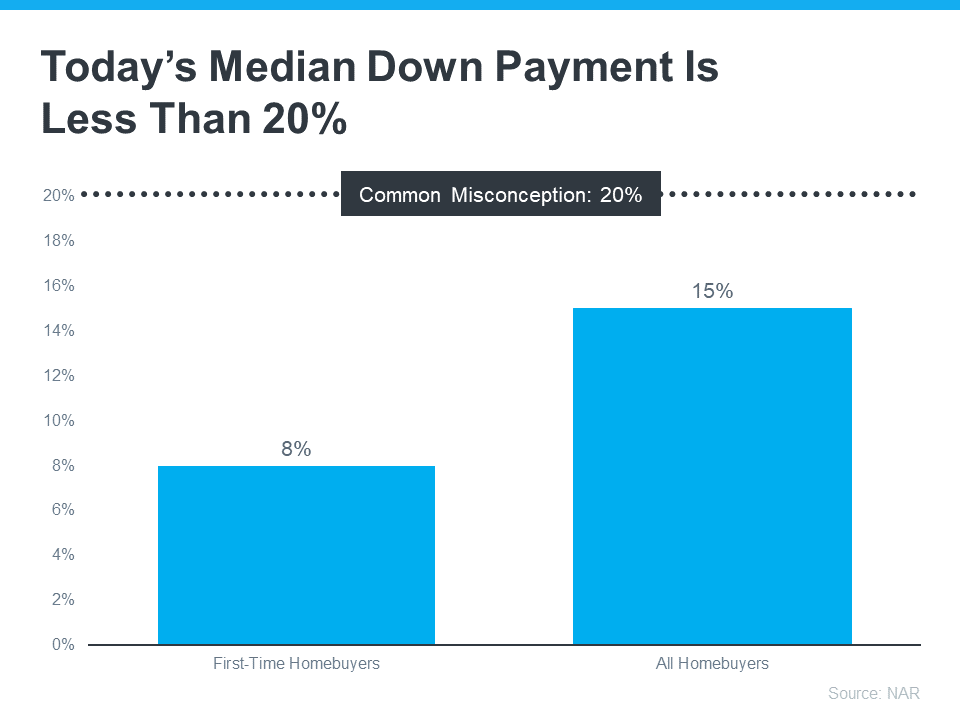

“Only 1.1% of mortgage holders (582K) ended the year underwater, down from 1.5% (807K) at this time last year.”And since homeowners are on more solid footing today, they’ll have options to avoid foreclosure. That limits the number of distressed properties coming onto the market. And without a flood of inventory, prices won’t come tumbling down. Bottom LineWhile you may be hoping for something that brings prices down, that’s not what the data tells us is going to happen. The most current research clearly shows that today’s market is nothing like it was last time.   If you’re planning to buy your first home, saving up for all the costs involved can feel daunting, especially when it comes to the down payment. That might be because you’ve heard you need to save 20% of the home’s price to put down. Well, that isn’t necessarily the case. Unless specified by your loan type or lender, it’s typically not required to put 20% down. That means you could be closer to your homebuying dream than you realize. As The Mortgage Reports says: “Although putting down 20% to avoid mortgage insurance is wise if affordable, it’s a myth that this is always necessary. In fact, most people opt for a much lower down payment.”According to the National Association of Realtors (NAR), the median down payment hasn’t been over 20% since 2005. In fact, for all homebuyers today it’s only 15%. And it’s even lower for first-time homebuyers at just 8% (see graph below): The big takeaway? You may not need to save as much as you originally thought.

Learn About Resources That Can Help You Toward Your GoalAccording to Down Payment Resource, there are also over 2,000 homebuyer assistance programs in the U.S., and many of them are intended to help with down payments. Plus, there are loan options that can help too. For example, FHA loans offer down payments as low as 3.5%, while VA and USDA loans have no down payment requirements for qualified applicants. With so many resources available to help with your down payment, the best way to find what you qualify for is by consulting with your loan officer or broker. They know about local grants and loan programs that may help you out. Don’t let the misconception that you have to have 20% saved up hold you back. If you’re ready to become a homeowner, lean on the professionals to find resources that can help you make your dreams a reality. If you put your plans on hold until you’ve saved up 20%, it may actually cost you in the long run. According to U.S. Bank: “. . . there are plenty of reasons why it might not be possible. For some, waiting to save up 20% for a down payment may “cost” too much time. While you’re saving for your down payment and paying rent, the price of your future home may go up.”Home prices are expected to keep appreciating over the next 5 years – meaning your future home will likely go up in price the longer you wait. If you’re able to use these resources to buy now, that future price growth will help you build equity, rather than cost you more. Bottom LineKeep in mind that you don't always need a 20% down payment to buy a home. If you're looking to make a move this year, let’s connect to start the conversation about your homebuying goals. |

Let's ConnectWith the correct person by your side, the buying and selling process doesn't have to be full of stress, doubt and anxiety - it can actually be FUN! Archives

May 2024

Categories

All

Jacquelyn Duke, Realtor®

Licensed to Sell in the State of Iowa Jacquelyn@SellingCentralIowa.com (515) 240-7483 Realty One Group Impact 617 SW 3rd Street Ste 101 Ankeny, IA 50023 Disclaimer: The material on this site is solely for informational purposes. No warranties or representations have been made.

|

RSS Feed

RSS Feed